In the coming weeks, we’ll be busy collecting receipts, following up on t-slips that have been misplaced and wishing that we could have done a better job of our tax planning. Unfortunately, by the time we’re in the middle of tax reporting, it may be too late to do much tax planning.

If there’s one lesson, it’s: “Know your tax bracket limit and stay within it”.

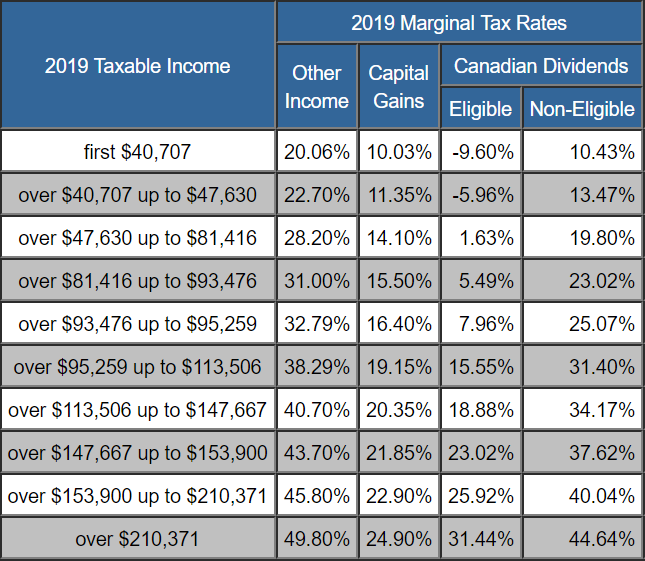

Every dollar that falls into the next higher tax bracket is subject to higher taxation. Tax brackets shift with inflation and in response to federal budgets. You can easily find the 2019 tax tables by visiting https://www.taxtips.ca/marginaltaxrates.htm and selecting the appropriate table for your province of residency. If you find your taxable income approaching the threshold to the next higher tax bracket, try some of these strategies:

1. Have your employer deposit bonuses, commission income and any other income that you don’t receive regularly into your RRSP (within RRSP contribution limits, of course). Ideally, your household budget should not bank on these unpredictable income streams so depositing them into your RRSP should not affect your standard of living. Furthermore, this strategy will allow you to deposit the full, pre-tax, amount to your RRSP resulting in a contribution that could up as much as 30% higher than if you had received the funds, and then made the contribution yourself.

2. Divert any non-registered funds to your TFSA or RRSP. Non-registered portfolios produce taxable investment income each year including interest, dividends and capital gains. The income can easily land you in a higher tax bracket than your employment earnings alone would. Using tax-exposed money to satisfy your TFSA or RRSP contributions means that you’re optimizing the annual taxation on your investment income.

**A word of caution: transferring assets between these accounts will be considered a “deemed disposition”. If any of those investments that have increased in value, this could trigger capital gains taxes.

To optimize the strategy, use depreciated assets for TFSA contributions and use appreciated assets for RRSP contributions. Depreciated assets should be sold prior to contributing the proceeds to your TFSA in order to crystalize the capital loss. Appreciated assets can be transferred in kind (i.e. in shares form or mutual funds units) and any capital gain crystalized will be covered by the deduction you receive for making the contribution.

3. Be strategic about claiming your RRSP contributions. The same way that taxable income will be subject to more tax if it falls into a higher tax bracket, an RRSP contribution will yield a higher refund if it is applied against income that is situated in a higher tax bracket.

Here’s an example. If you live in British Columbia and earn $120,000 per year and want to make a $10,000 RRSP contribution, the relevant tax brackets are marked below. (source: www.taxtips.ca). If you claim the full $10,000 RRSP deduction in one year, your refund would be approximately $3,985. However, claiming only enough to drop your taxable income to the 38.29% bracket ($6,494) and carrying the balance forward ($3,506) to be claimed in the 40.70% bracket again in the following year will add $315 to your refund.

4. Be strategic about harvesting your wealth. For those who are retired and using their wealth to supplement their federal and workplace pensions, the same principal can be applied. If you need to supplement your CPP, OAS, workplace pensions and minimum RRIF payments to cover your expenses, consider drawing the money from a combination of TFSAs and non-registered accounts. The withdrawals from TFSAs are non-taxable and withdrawals from non-registered accounts will be taxable to varying degrees; but are likely to be much more lenient than withdrawing additional sums from your RRIF. Furthermore, if your taxable income is likely to exceed $77,580 after implementing retirement income splitting, taking funds from your TFSA and non-registered accounts may also help you to preserve your OAS from being clawed back.

They say that there are only two certainties in life; death and taxes. I say, at least one of them can be controlled.

{kind=link}